James McDonald, Managing Editor, WARC Data, provides three scenarios in which the spread of the COVID-19 virus may potentially impact purchasing, media consumption and advertising investment.

Last week we published our latest projections for global advertising investment, which predict a 7.1% rise in dollar terms (5.6% underlying growth) to $659.6bn this year.

This forecast may seem overly dovish given the ongoing concern around the unfolding novel coronavirus (COVID-19) outbreak, so we felt it prudent to provide additional context around the potential ramifications of the spread of the virus based on the information we have to date.

The outbreak has already impacted business decisions and budget commitments in Asia. Whether this trend sustains and replicates in other markets depends on how well the virus is contained, but three broad, hypothetical scenarios relating to the impact on media activity can already be ascertained.

Before exploring these, it is worth assessing the potential effect of COVID-19 on consumer-facing businesses. This can be been gauged, to a degree, by a study of the Severe Acute Respiratory Syndrome (SARS) outbreak in the first half of 2003 and the Middle East Respiratory Syndrome (MERS) outbreak between May and August 2015.

Consumers are most likely to cut back on luxuries, entertainment and leisure activities

Out-of-home entertainment suffered badly in the SARS period across China, Taiwan and Hong Kong, with a large decline in eating out, both in fast food and full-service restaurants, TNS data show.

Other out-of-home activities such as visiting bars and cinemas also decreased substantially. During the MERS outbreak, cinema audiences were down 55% in South Korea, with similar rates recorded among attendances at amusement (-54%) and water parks (-56%).

Retail establishments were also hit during the SARS period, but to differing degrees. A tendency to stock up on the essentials saw fewer shopping trips, particularly in China and Taiwan, while quick visits to convenience stores largely safeguarded them from major decreases.

Shopping for non-essentials dipped across all three markets, especially at malls and department stores, with the most severe negative figures in Taiwan (-44%), but also in China (-38%) and Hong Kong (-30%).

Much of consumer spending moved online. In South Korea, online sales were up 27% for Lotte Mart during the MERS outbreak, compared to a 10% fall at its brick-and-mortar outlets. Online sales were also up markedly for E-mart (+63.1%) and Home Plus (+48.1%).

A similar trend can be observed in consumer reaction to COVID-19. Data from Yimian, a sister company of WARC, show substantial growth in the purchase of healthcare items on Tmall between 19th January and the 9th February. Sales of surgical masks totalled 107.2m (compared to 587,177 the previous year), with sanitisers (+3271% year on year), vitamin tablets (+3171%) and disinfectant (+2673%) also selling rapidly.

A Wavemaker survey, conducted last month, found that 68% of Chinese consumers have not cut back on their spending in light of COVID-19, while 83% still pay for the essentials as they did before.

A Wavemaker survey, conducted last month, found that 68% of Chinese consumers have not cut back on their spending in light of COVID-19, while 83% still pay for the essentials as they did before.

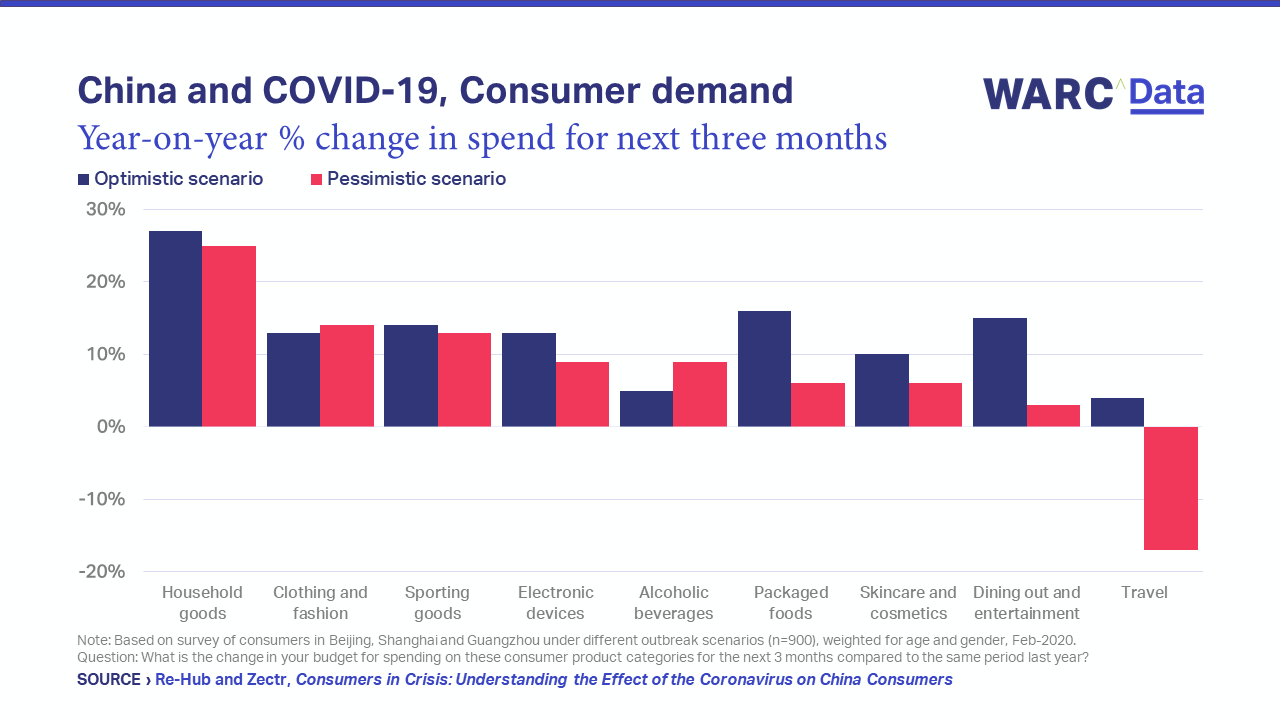

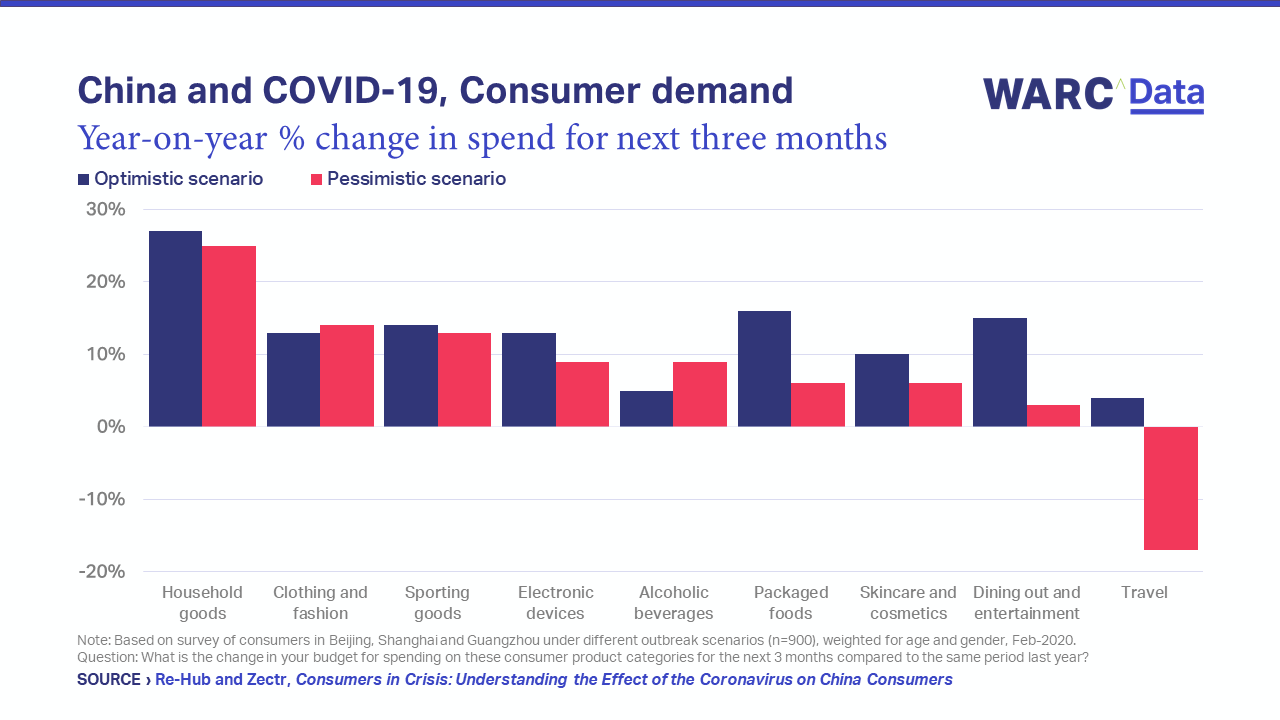

But projections by retail platform Re-Hub and insights provider Zectr, based on their survey of consumers in Beijing, Shanghai and Guangzhou, suggest travel, restaurants and entertainment businesses are likely to witness lower levels of consumer spend in the coming months. This mirrors the trends observed during the SARS and MERS outbreaks.

Scenario planning in response to COVID-19

COVID-19 has already spread faster and further than both SARS and MERS, and the human cost is, at the time of writing, already three times greater.

We have seen evidence to suggest that brands are adopting a cautious approach to committing budgets in the first quarter of the year. The severity of the slowdown in investment will become clearer as new market data are released next month, but we do have indications today, and these have led us to present three broad scenarios for the impact of the virus on advertising investment over time.

Scenario one: spend is displaced but full-year growth is largely unaffected

The virus is contained, and displaced budgets are reallocated towards the second half of the year. This could, however, push up costs as competition for inventory intensifies. This is the scenario on which our current projections are based.

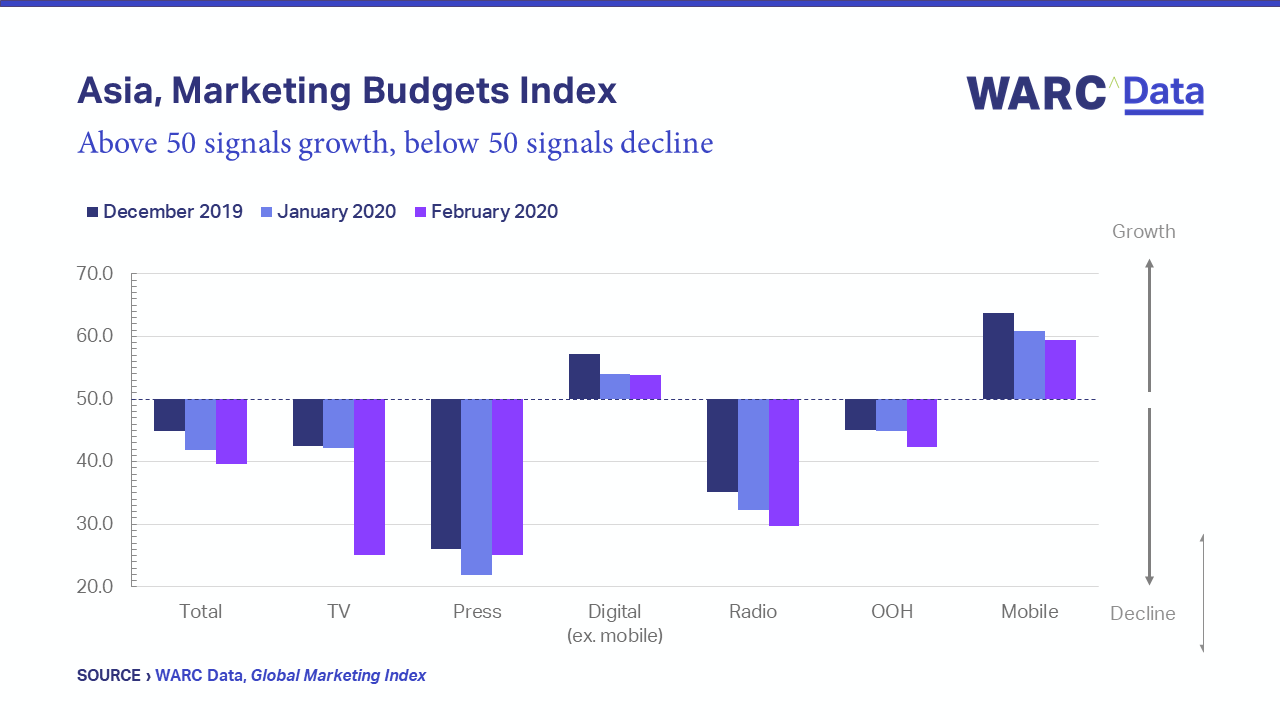

WARC’s Global Marketing Index, a monthly barometer of practitioner sentiment towards trading conditions, marketing budgets and staffing levels, shows that budgets were tightened in APAC last month, with an index value of 40.7 the lowest in its seven-year history (a value below 50 is indicative of decline). The survey data show that traditional media recorded the worst dips in Asia, while digital growth was notably slower than had been seen previously.

Guidance from Baidu, issued last week, suggests income could be down by between 5% and 13% in the first quarter of 2020, equivalent to $444m. Weibo stated its revenue could fall by as much as a fifth, or $79.8m. Both companies stressed it was too early to be certain.

Guidance from Baidu, issued last week, suggests income could be down by between 5% and 13% in the first quarter of 2020, equivalent to $444m. Weibo stated its revenue could fall by as much as a fifth, or $79.8m. Both companies stressed it was too early to be certain.

Scenario two: spend is reallocated significantly as brands focus on the short-term

Heightened restrictions – beyond those already announced – are placed on movement and large gatherings in multiple countries and territories. Cinema is susceptible to lower audiences, and the out-of-home market conceivably suffers from lower reach – particularly in transport locations. Radio, core to the commute, is also left somewhat exposed.

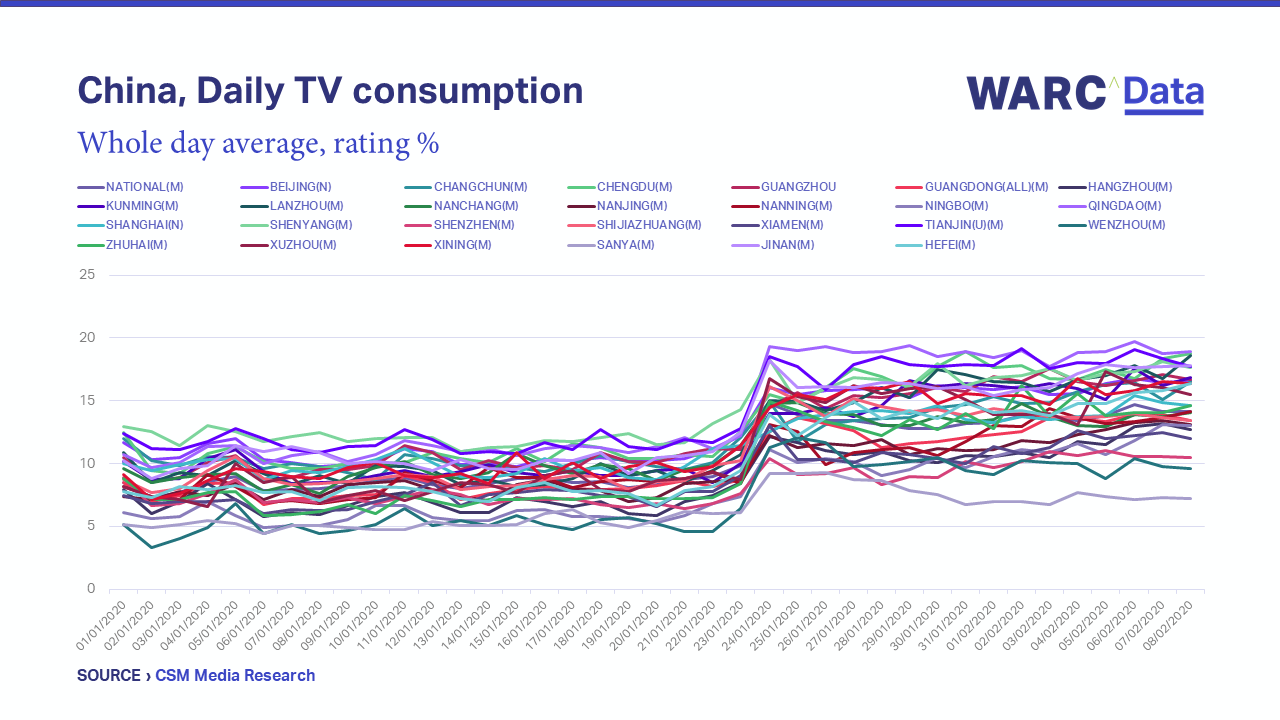

Conversely, an increase in self-isolation leads to an uptick in TV consumption, as has already been observed in China – in some cases 50% above the daily average. Consumption of AVOD services and other online video also rises, most notably among younger audiences. Over two-thirds (70%) of the Chinese respondents to Wavemaker’s survey said they are watching more TV and video content than before – four-fifths (83%) are reading more news.

Social and messaging investment may rise ahead of organic rates in Western markets alongside increasing usage as people keep in touch with family and friends, though the correlation between social impacts and advertising spend is moot. In-game adspend growth has the potential to reach triple figures, but from a comparatively low base.

Social and messaging investment may rise ahead of organic rates in Western markets alongside increasing usage as people keep in touch with family and friends, though the correlation between social impacts and advertising spend is moot. In-game adspend growth has the potential to reach triple figures, but from a comparatively low base.

This scenario must be taken with the added caveat that shifts in consumption will not translate directly into shifts in marketing strategy. Brands may continue to apply caution before committing spend, particularly among sectors which rely heavily on Chinese supply chains.

That said, a prolonged disruption and a risk of lower consumer spending will result in many advertisers delaying big brand work, instead favouring a tactical retreat into performance marketing. This would be pertinent during the Easter period in the West, for example, with retailers and CPG brands in particular focusing on discounting and promotions to stave off any lag in sales.

If e-commerce volumes rise, it is conceivable that investment is focused in digital advertising to facilitate the path to purchase, particularly in the channels that are closest to consumer decision-making (such as paid search and social platforms with a commerce element, like WhatsApp). This course of action is most likely among advertisers that adopt attribution modelling.

A renewed focus on short-termism across the board may scupper the desire to pivot back to brand, that was observed in WARC’s Marketer’s Toolkit 2020.

Scenario three: severe disruption heightens the potential of an advertising recession

The outbreak removes one percentage point from global GDP, per Nomura projections, as major economies skirt with or fall into recession. Large urban areas are locked-down for prolonged periods (three-quarters – 74% – of Britons support the quarantining of cities to prevent the spread of the outbreak, compared to 70% of Americans and 62% of Germans, per Ipsos MORI), and major sporting events are either postponed or cancelled.

In this scenario, the likelihood of the global advertising market falling into recession is higher but is not guaranteed – ad expenditure’s relationship with GDP is fairly strong, with a correlation coefficient of 0.62 over the last decade, though this is weakening as the industry migrates online (internet adspend has grown six times faster than the global economy over recent years).

Alphabet, Facebook and Amazon stand to gain from a renewed focus on delivering short-term marketing goals in a crisis period, but a sizeable amount of their income relies upon small and medium sized enterprises, and these are the advertisers that are perhaps most vulnerable to a sharp economic downturn.

The cancellation of events such as the UEFA Euro 2020 football tournament – the first to be held across multiple European countries – and the Olympic and Paralympic Games, is most likely to have an adverse effect on traditional media (the Olympics lifts TV spend by close to a billion dollars in the US alone) but will also impact online publishers and BVOD platforms.

In a briefing note this week, Brian Wieser, Global President, Business Intelligence, GroupM, rightly reiterated the need for marketers to prepare credible alternatives as they develop marketing strategies – this is particularly true for big brand moments around events like the Olympics. WARC research shows such practice enables agility and fosters innovation.

For brands and media owners, scenario planning should now be top of the agenda.